Rates Up, Balances Up: Uneven Transmission of Monetary Policy in Consumer Credit Markets

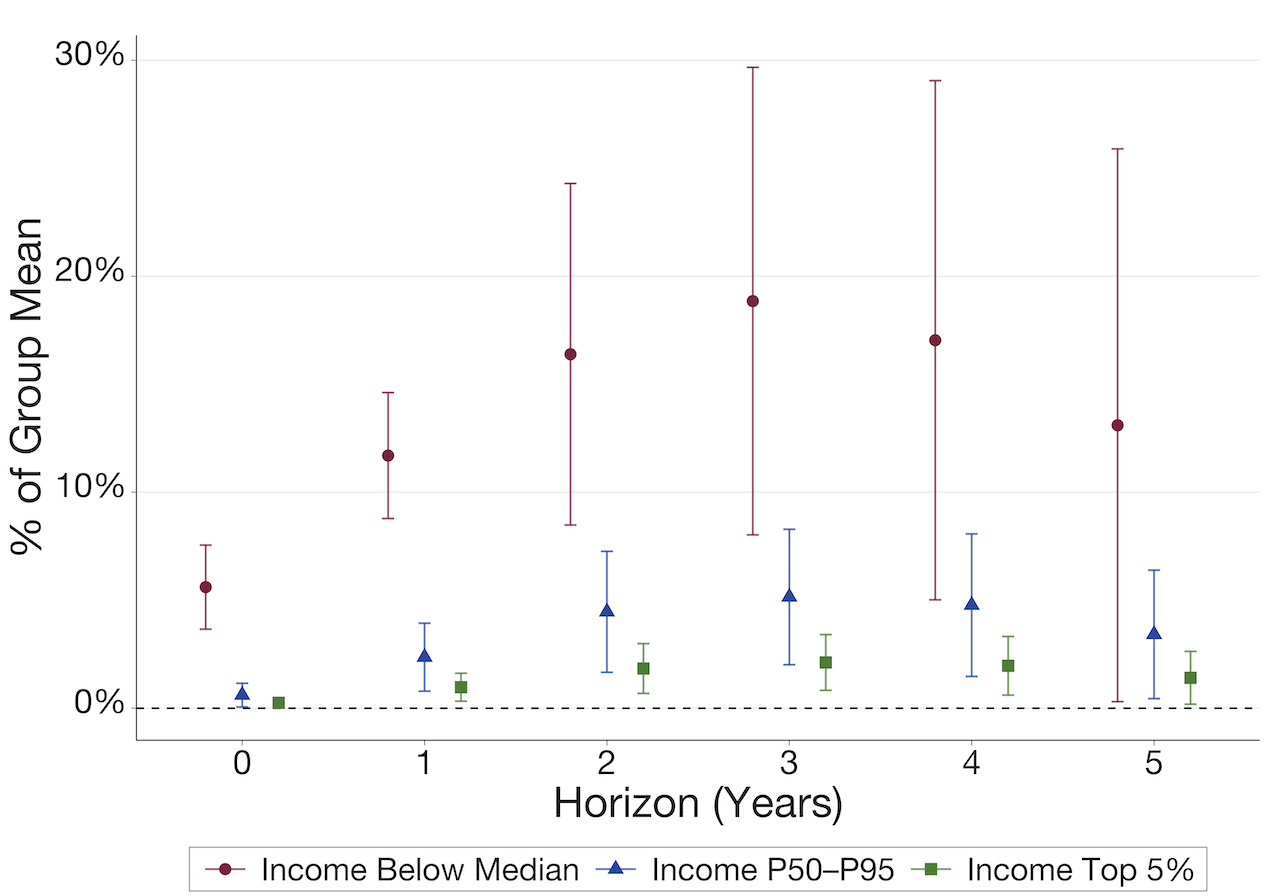

This paper looks into the heterogeneous transmission of monetary policy to households’ debt balance.

This paper looks into the heterogeneous transmission of monetary policy to households’ debt balance.

Developing a DSGE model with heterogeneous investors facing financial frictions to study capital reallocation and misallocation.

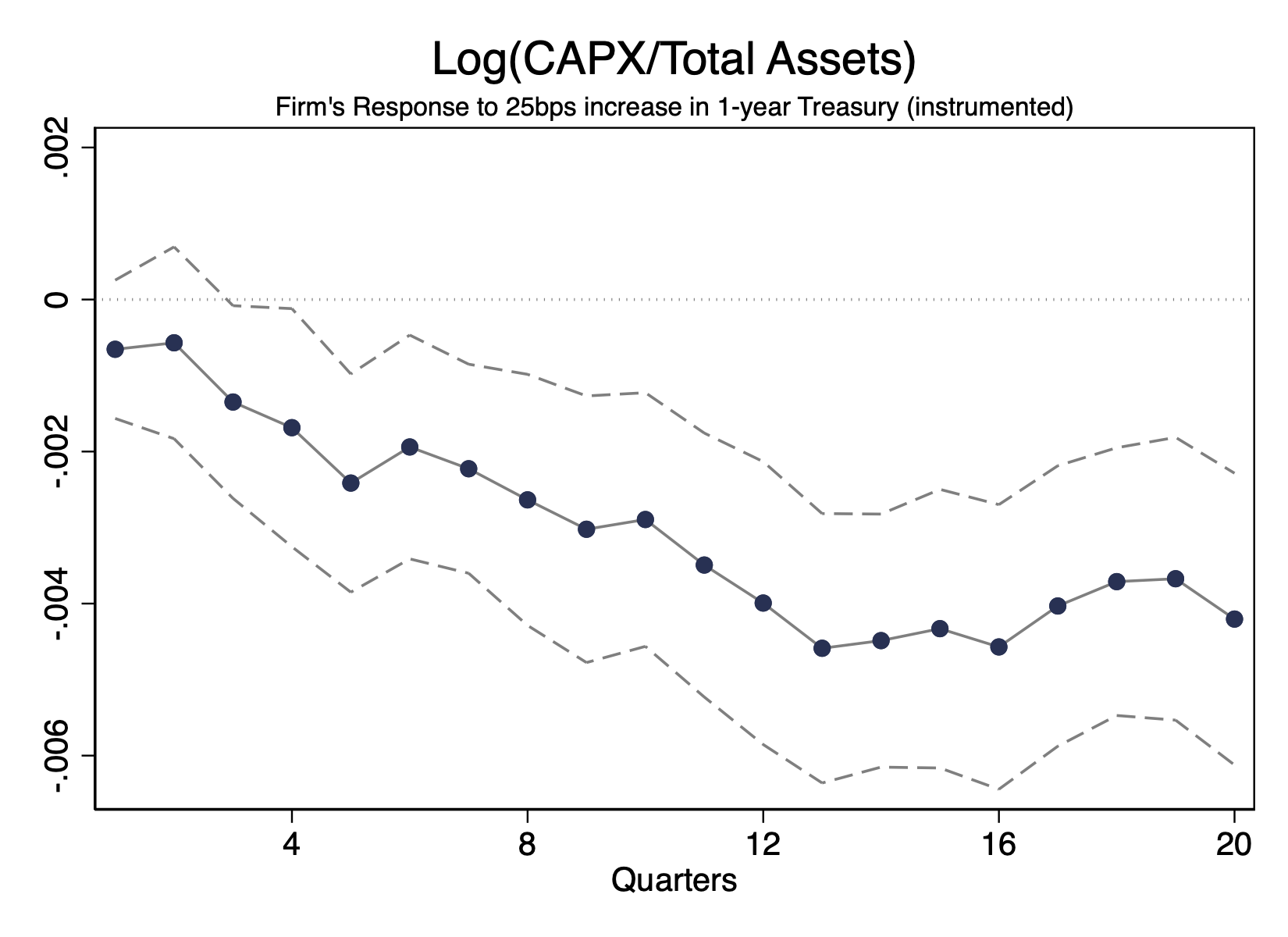

This paper highlights the role of the equity financing constraints in the transmission of monetary policy.

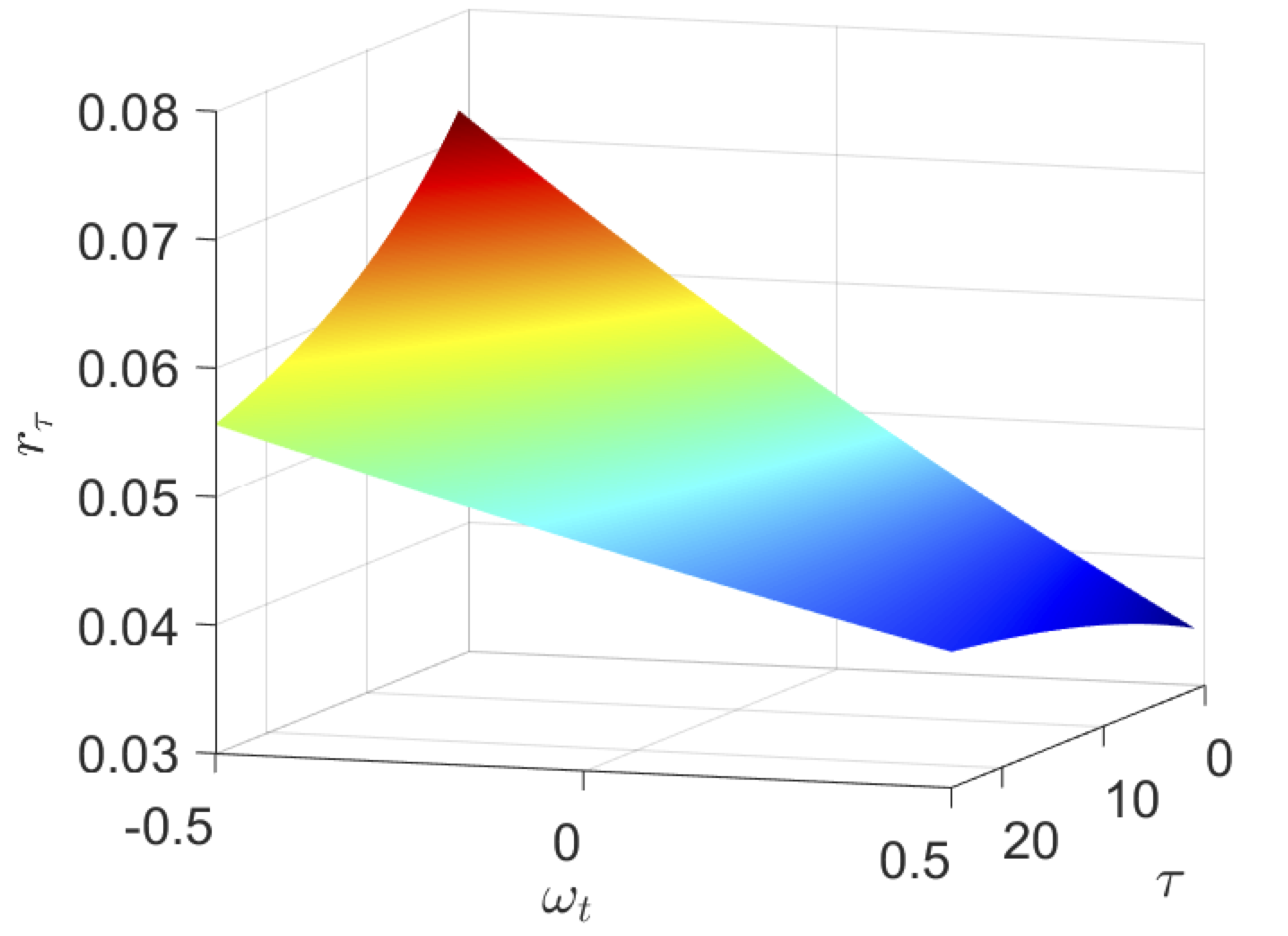

This paper studies a general equilibrium model with heterogeneity in both risk aversion and beliefs about the expected growth rate of the aggregate endowment.